Sometimes we can’t really know a thing from a distance. Often, it’s impossible to really experience the truth of a thing until we get close, or even all the way inside it.

When we start to really get inside something, we start to see it for what it is, not what we thought it would be. Sometimes that’s really cool and amazing and we love it. Other times it starts to get dark and awful. Sometimes we push through because we’re going to finish what we started. Other times we reevaluate and make new decisions. It can be hard to know which way to go; to know if we should hold ’em or fold ’em.

I had a dream of being an attorney since I was a kid. I like to argue and wrestle with abstracts (Ok I like when people listen to me talk too). But being a lawyer is probably nothing like the lawyers I see on the TV shows. I’ve heard and read enough stories of attorneys walking away from practicing law that I probably would not have been happy. Maybe some things are better left dreamed about.

This blog post will be a little different in some ways. It’s a bit of the same in that I’m putting out there our financial plans and where we are so far. It’s a bit different because I’m hoping to get a bit more personal. I’m going to be a little more open about how we fared on selling the House of Wales; not in an attempt to boast as much to help anyone else that might be following.

So let’s just dive right in. Through years of hard work, consistent upkeep, smart upgrades, and market timing, we did very well selling the House of Wales. It’s been one of the major decisions in our lives; not just because we sold the house but also because we changed lifestyles. When all was signed and done, we sold for about $130K more than we owed.

That’s not counting paying off the Baby House, which took about $40K from that profit (debt free Baby Howwwse!) That’s also not counting fees, some upgrades, and other associated costs from the process of selling (If you ever need a realtor, seriously, please contact me), so we put about $70K in a money market fund account until we could settle on the exact plan.

Our current plan was to be debt free by October 1st 2020. We made this plan before we decided to sell the House of Wales. We were killing it. We had our debt whittled down to just three more loans: the car ($20K), the truck ($20K), and my school loan ($25K) and were throwing gobs of money at them every month.

We had originally planned to invest the entire profit and leave it for 10-15 years while we added to it slowly and continued our October 1st 2020 debt free pursuit.

A few weeks ago, like we always do, we began checking down the action plan and reviewing the timing. In other words, we got a very close-up view of our options. One of us (not sure which one) said, “And we’re sure we’d not be better off finishing the debt free journey and then starting to invest?”

Sidebar: You know how when someone asks a question and it’s more than a question and then the person says something like what? I’m just asking only you know their actually not just asking and everything kind of starts to unravel?

Uh huh.

Like that.

(Insert open can of worms).

We started reviewing our options again, making sure of our choice. It really came down to two options: invest 100% of the profit or get clear of 100% of the debt. Right now.

We talked about it alot.

A-lot.

The cool thing about talking about something alot is that often it serves as a catalyst to review other areas of life: plans, dreams, the future (and to have another martini. Gin, of course). It helped us boil down what we were really chasing.

Paying off debt cuts stress and creates a sense of freedom. It takes away some of the “have to’s” of life. Living expenses don’t go away, but the financial drag of payments and interest does. It also creates a really cool sense of accomplishment.

Someone once told me that it’s not how much money we make; it’s how much debt we have. If we don’t have any debt, we don’t need much money. (Just enough, really, for a 1-week trip on a cat in the Bahamas. Every year. With martinis).

Being debt free makes good sense and is never a bad idea.

We also knew we could use the $70K as a quick-start towards creating passive income through investing that would add to my two pensions; one from the Coast Guard (already drawing that one) and one from the state when I eventually stop full-time work. I plan to add another 5-7 years of state employment before taking that step.

Those pensions will create a bedrock income for retirement for the rest of my life (~$3K per month) before any passive investment income and before social security (no plan yet on when to draw). A cool additional benefit of my Coast Guard service is lifetime healthcare (huge, I know).

Rachel also has a 401K that’s worth about $40K right now that we’re also deciding how best to grow.

The investment idea was intriguing because we’re late to that game. I’ve let the awareness of my pensions make me lazy. I also liked the investment idea because I wanted to ride up and down the condo elevator checking my portfolio and saying cool things like “oh yeah, diversified” and “market share” and “Dude this ROI is toasting my nuggs.”

Yes, we would still have time time to invest but we’re losing the amount of wealth a $70K chunk could jump start (and my elevator trips wouldn’t be nearly as cool). It might take us a few years to build that core amount back into an investment with our income. Although we really don’t see ourselves coming to full-stop retirement until we’re really old (like 116), it might be hard to hold down full time work from a 40′ cat in the Bahamas.

When it came right down to it and we could really see everything up close, we decided to bring home the prize that we started chasing 9 months ago:

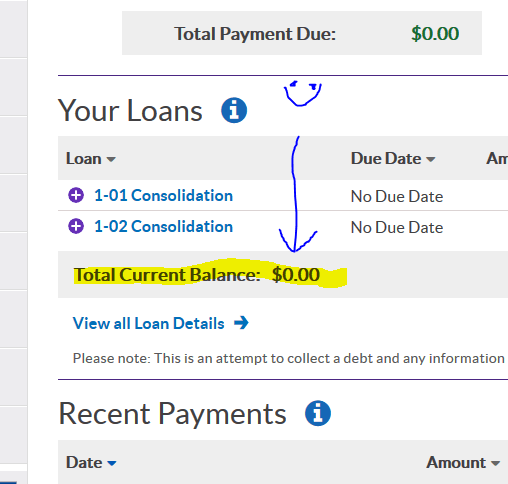

We’re Debt Free!

Happy Birthday to me!

When we started our debt free journey in January of 2019 we had NO idea what would become of this adventure. It’s been quite the ride!

It hasn’t really sunk in yet. I keep going to the school loan website and flipping it the bird while laughing and dancing around in little circles (I also have a little song I made up but it’s mostly naughty words). It’s fun to keep seeing zeros. It’s a huge chapter finally closed. I might keep doing my dance for awhile (probably close the shades next time though).

It’s the same with the vehicles. That’s not as fun though because we paid by e-check (and I don’t have a song made up for those). Still, the sense of there, that’s finally over feels really good (I might drive past the dealerships and flip them a bird too).

I think we’re going to live in this for awhile.

Small, quiet, 4th floor balcony celebrations are the best.

I guess I’m going to have to find something else to write about.

I don’t think that’s going to be too hard.

I’m proud of us.

Debt free Middle Age life feels really, really good.